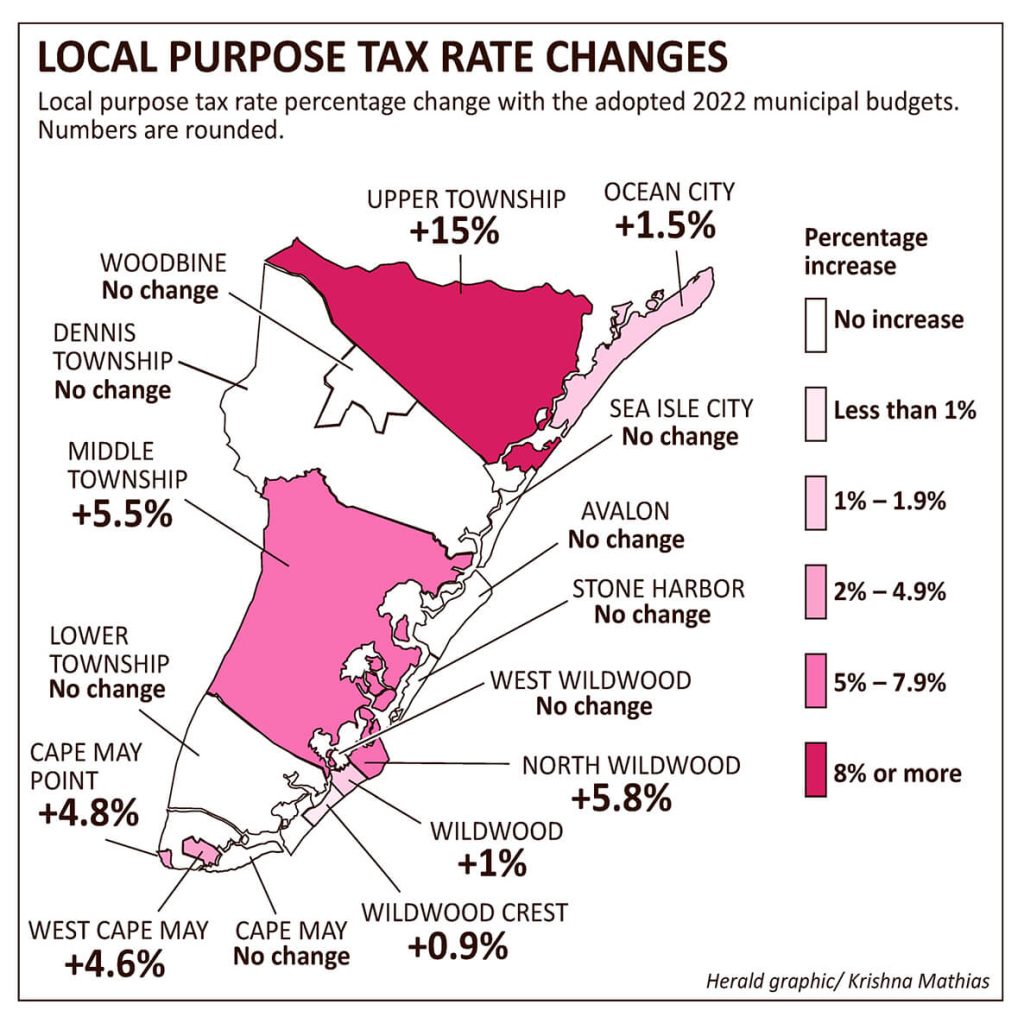

CORRECTION: The above graphic incorrectly stated that North Wildwood had a local purpose tax rate increase of 5.8% in 2022. The actual increase was 3.6%.

COURT HOUSE – Each year, the county’s 16 municipalities adopt budgets in the spring, with some stretching into early summer. This year, half – eight out of 16 – of those towns enacted increases in their local purpose tax. Eight held the line and adopted budgets with no change to the tax rate.

Those with tax increases were Upper Township, Middle Township, Ocean City, North Wildwood, Wildwood, Wildwood Crest, West Cape May, and Cape May Point.

The municipalities whose budgets did not include a hike in the tax rate were Dennis Township, Lower Township, Woodbine, Sea Isle City, Avalon, Stone Harbor, West Wildwood, and Cape May.

Local Purpose Tax Rate

The bottom line for many taxpayers is the local purpose tax rate. Among those who increased their tax rate this year, Wildwood and Wildwood Crest both enacted an increase of less than 1%. The largest increase was in Upper Township’s 2022 budget, which contained a 15% hike in the tax rate.

For some towns, a tax increase was unavoidable, even with significant revenue from the American Rescue Plan (ARP).

In Middle Township, $981,000 in ARP funds was not enough to head off a 5.5% increase in the tax rate. Upper Township also had the benefit of $485,000 in ARP funds in the 2022 budget.

In Ocean City, the increase in the local purpose tax rate was explained as required due to an unexpected increase in the fees for solid waste removal.

Ocean City is serviced by Gold Medal Environmental, which, citing an inflationary increase in fuel and payrolls, approached each of the municipalities with which the company had existing contracts, seeking additional funding, and even threatening to leave trash uncollected, as the busy summer began.

Among the municipalities that were able to adopt budgets with no increase in the tax rate, one – Stone Harbor – was recovering from a 2021 budget where a series of pressures, including an emergency appropriation from 2020, left the borough with an over 8% hike in the tax rate.

In some budget documents, it was unclear how the municipality managed to avoid a tax increase. In Woodbine, the budget is supported by the use of $420,500 in general fund surplus dollars. Yet, the official budget document available on the borough’s website shows a deficit in the surplus balance, which is the source of the funds used. Attempts to get an explanation from the borough’s chief financial officer have not yet resulted in a reply.

Comparing Budgets

Comparing budgets is a difficult task given that six of the municipalities do not make use of self-financing utilities, meaning that funds and expenses that would flow through a water, sewer, or beach utility in one town are included in the general fund budget of a municipality that does not make use of a utility.

There are a couple of statistics that may provide a modicum of comparative insight.

The general fund surplus is the accumulation of previously budgeted funds that were unspent and saved. Each municipality makes use of its surplus balance to offset appropriations in any given year’s budget. The surplus used is intended to be replaced in the general fund balance based on estimates of savings that are expected over the course of a year.

When anticipated revenues do not materialize or unexpected expenses intrude on a budget, these can threaten the budget’s ability to replace the surplus used at the end of the year. Several towns saw their accumulated general fund surplus balance decline during the pandemic when revenue streams were interrupted.

In 2022, the percentage of total surplus funds used to balance the annual budget varied substantially. Among the highest users of surplus funds for balancing the budget were Upper Township, which used 92% of its fund balance in the 2022 budget, and both Middle Township (78%) and West Wildwood (73%).

Four municipalities came in with budgets that made use of less than 35% of their start-of-the-year fund balance. They were Cape May Point (33%), Dennis Township (34%), Wildwood Crest (35%) and Cape May (35%).

One measure of financial strength is the size of the start-of-year surplus balance, which provides a cushion against unexpected events. Seven municipalities started 2022 with fund balances of over $7 million. These towns were led by Ocean City and Wildwood Crest, both with balances of over $10 million.

Following them were Cape May ($9.8 million), Lower Township ($8.6 million), Sea Isle City ($8.1 million), Avalon ($7.9 million), and North Wildwood ($7.1 million).

Towns with $5 million or less in the general fund balance are Wildwood($5 million), Stone Harbor ($3.1 million), Middle Township ($2.2 million), Dennis Township ($2 million), Upper Township ($1.8 million), West Cape May ($1 million), Cape May Point ($550,000), and West Wildwood ($426,000).

This list does not include the deficit shown on the posted 2022 budget for Woodbine, which may be the result of an error in the composition of the budget.

Debt

Among the towns, another potentially useful way of looking across budgets is considering the percentage of the general fund budget that is appropriate for debt service payments.

Even with $5 billion in assessed property valuation, Stone Harbor leads all 16 municipalities, with 21% of its general fund budget allocated to debt service, better than one in every 5 budget dollars. Other municipalities that share a high ratio of debt service dollars to total budget are Sea Isle City, at 20%, and Ocean City and West Wildwood, both at 19%.

The towns with the lowest level of general fund appropriations allocated to debt service are led by Avalon, at 0.48%, and Cape May Point, at 0.69%. Among the larger towns, Middle Township is at 5% and Wildwood sits at 6%.

Other Revenue

County municipalities show wide variance in revenue streams other than taxation. One measure of this is the degree to which a municipality’s general fund budget is dependent on tax dollars.

The values range from a high dependence in West Wildwood, where 77% of the general budget is funded by the tax levy, to a low of 15% in Woodbine.

Among the larger municipalities, Stone Harbor has the highest dependency on taxation, with 73% of all revenue in the general fund budget coming from taxation. In contrast, Cape May’s taxation represents only 48% of total general fund revenue.

In these cases, Stone Harbor has not moved to develop certain revenue streams that bring significant revenue to Cape May. A good example is the use of the occupancy tax in Cape May, where the 3% tax has just been extended to cover online short-term transient rentals through apps like Airbnb. Stone Harbor is one of many of the county’s municipalities that have chosen not to impose the occupancy tax as a municipal user tax.

With the exception of Cape May, the shore towns from Ocean City to Cape May Point all have budgets that depend 60% or more on tax revenues.

On the mainland, Lower Township’s tax revenue is 72% of all general fund revenue, while Upper Township has a tax revenue ratio of only 27%, due mainly to the large state aid it receives made up almost entirely of energy tax receipts from the decommissioned B.L. England generating station.

Similarly, Dennis has a low ratio, at 38%, due to its share of energy tax receipts revenue from the state.

Middle Township is midway between Upper and Lower in its dependence on taxation. Middle’s 2022 budget requires tax revenue for 58% of total revenues, but that percentage was helped by the large infusion of ARP funds mentioned earlier.

Middle will also be facing a new problem in 2023. An error in the preparation of the 2022 budget has forced the municipality to enact an emergency appropriation of $345,000 to cover its required payment to county central dispatch. The emergency appropriation must be provided for in full in the 2023 budget.

County

In 2022, the county adopted a budget that had no tax increase. The county’s 2022 budget depends on taxes for 75% of its total revenue.

Its $200 million budget has $22 million in debt service for 2022, about 11% of the total monies appropriated.

The county uses about one-third of its surplus each year, offsetting budget appropriations. It started 2022 with a surplus of almost $36 million.

To contact Vince Conti, email vconti@cmcherald.com.