ED. NOTE: For online subscribers, the Herald will publish more in-depth looks at some of the municipal 2023 budgets. The first of these is online and examines Stone Harbor’s budget. Which town’s budget should we examine next? Let us know by emailing newsdesk@cmcherald.com.

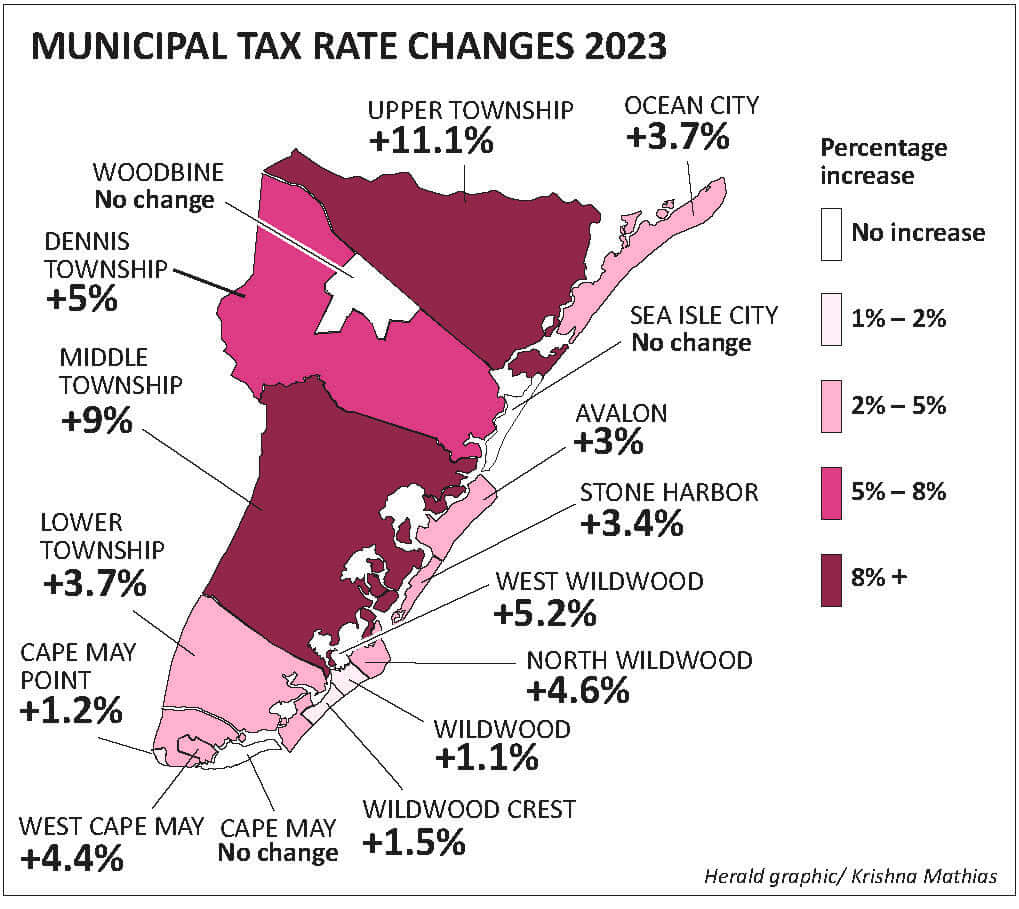

COURT HOUSE – All but three of Cape May County’s municipalities increased the local purpose tax rate in their 2023 budgets. For those that increased, the range ran from a bit over 1% in three towns to 9% in Middle Township to just over 11% in Upper Township.

This was a year when several variables came together in a perfect storm to test the financial strength of local municipalities across the county.

The year began with a persistent high national inflation rate impacting the purchases of goods and services for municipalities just as it did the general public.

This year also marked the end of the historic levels of federal pandemic relief to municipalities that was intended to help off-set short-term losses in revenue in local budgets. In some towns, the funding was seen as an infusion of revenue that allowed spending that was not temporary. When the funds ran out, the budgets were left with gaping holes.

To make matters worse, the Murphy administration allowed a historic jump in employee health care premiums, then settled with state employee unions and left the spike in costs for county and municipal workers as a local government problem. Pension costs, also set by the state, went up as well, leaving many municipalities with expenses they could not cover without tax increases.

Island Municipalities

In the far north of the county, Ocean City’s $99 million general budget required an increase in the local purpose tax rate of 3.7%. The city dealt with the state health care premium hike by changing to a private provider. User fees for parking and beach tags were increased. The city did not strain its surplus balance, using only 51% of the available balance as budget revenue.

The surplus balance is the accumulation of unspent funds from previous budget years. A percentage of it is routinely applied to new budgets to hold down or eliminate possible tax rate increases.

Ocean City has financial strengths to fall back on in hard times. The budget boasts a valuation level of over $12.5 billion, a general fund surplus in excess of $11 million, and a healthy cap bank of $7.2 million.

The cap bank is created when a given year’s budget is set at a level below the state’s 2% cap limit. The amount below the limit can be backed for three years and used if the municipality ever needs to exceed its cap in a specific year.

Moving down the coast, Sea Isle City is one of three municipalities that did not raise its local purpose tax rate this year. The town adopted a $28.5 million general fund budget and a $10.3 million water and sewer utility budget.

While the town boasts a strong surplus balance – at $8.8 million – and healthy user fee revenue in some areas – beach tag fees are anticipated at $1.4 million – the budget is exposed to reliance on taxpayer dollars; $2 out of $3 of revenue in the 2023 budget comes from the tax levy and the surplus used is another 16% of anticipated revenue. That adds to 82% of the expected budget revenue coming from either taxes or surplus.

Stone Harbor’s $5 million in debt services makes it, once again, the municipality with the highest ratio of debt service payments to general fund revenue.

Avalon cleared its books of all long-term general obligation debt in recent years. The borough’s $36 million general fund budget contains $4.7 million in library taxes. Like Ocean City, Avalon maintains its own library and is not part of the county system.

For the first time since 2016, Avalon’s budget called for an increase of 3% in its local purpose tax rate. The budget also made use of $5.3 million in surplus out of a total of $7.5 million.

Avalon has a water and sewer utility budgeted at $8.1 million and a beach utility with a budget of $2.1 million. Utilities can be used to transfer potential taxpayer liabilities into user-fee-supported activities. They must be self-financing.

The borough is in strong financial position with a high cap bank balance, low debt service, and roughly $4 million allocated to pay-as-you-go capital improvements.

Stone Harbor’s general fund budget includes a 3.4% hike in the local purpose tax rate. The $21.5 million operating budget makes use of 64% of the borough’s total $4.1 million surplus, up from 52% the prior year.

The budget is heavily dependent on the tax levy at $15.1 million and the use of surplus dollars because there are few alternative sources of revenue. Only 17% of the general revenue comes from sources other than taxpayer dollars or surplus, with the largest alternative sources of revenue being beach tag sales and parking.

The borough’s $5 million in debt services makes it, once again, the municipality with the highest ratio of debt service payments to general fund revenue. Overall, 23% of anticipated revenue is budgeted for debt service payments.

The borough has a water and sewer utility budgeted at $5.6 million, with $4.3 million budgeted in anticipated user fee revenue.

Click here for a more in-depth look at Stone Harbor’s budget.

North Wildwood is one of several county municipal budgets that do not make use of self-financing utilities. The $36.8 million 2023 budget contains a 4.6% increase in the local purpose tax rate.

The budget calls for tax levy revenue of $23.4 million. The nontax revenue looks large at $9.7 million, but most of that is sewer rents of $5.3 million that run through the general budget. The budget this year had to cope with the loss of $400,000 in Covid relief funds that had been available for the prior two years.

For North Wildwood, the biggest area of budget uncertainty is most likely tied to the city’s ongoing struggles with the state Department of Environmental Protection (DEP) and the costs of maintaining its beaches.

Wildwood managed to reduce the expected tax increase in its introduced budget to a final hike of 1.14%. The city has separate water and sewer utilities that have combined 2023 budgets of just under $17 million.

Of the county’s island towns, Wildwood has a relatively low valuation base at $1.4 billion, but does benefit from state funding at $1.1 million and urban enterprise assistance at $1.4 million. There was a noticeable increase in debt service, which climbed to $3.4 million from $2 million in 2022.

West Wildwood’s $3.5 million budget is over 75% dependent on tax revenue. The budget is close to 90% funded by a combination of the tax levy and the surplus used. There are very few other sources of revenue.

The 2023 budget calls for a 5.24% increase in the local purpose tax rate. In addition to the general fund budget, the town has a sewer utility budgeted at $880,000 and in which 21% of revenue goes to sewer utility debt service.

Wildwood Crest had one of the lowest increases in the local purpose tax rate at 1.45%. The municipality makes use of no utilities, so everything runs through the $27.5 million general fund budget.

The budget shows strong protections against unexpected problems, with the third highest surplus balance at the start of the year – $9.8 million – of which it used a low 37% to balance the 2023 budget.

Cape May required no tax increase in 2023. The $23.8 million general fund budget is helped by the use of three utilities. The utilities cover water/sewer and beach and tourism areas, with combined budgets of $9.2 million, all self-financing.

The municipality has the lowest level of taxpayer reliance for its general fund budget among the island communities at 45%. It also has the largest surplus balance at $12.7 million, of which it uses less than one-third for balancing the 2023 budget.

A major source of revenue for the city comes from shared service arrangements with the Coast Guard and the other two island municipalities. The city makes use of a citizen advisory committee that has helped identify alternative revenue sources.

Cape May Point is a small municipality with the lowest general fund budget – at $2.2 million – in the county. The town also maintains a water/sewer utility budgeted at $900,000.

In 2023, the budget calls for a 1.2% increase in the local purpose tax rate. The municipality is heavily reliant on tax revenue – at 74% of the total general fund revenue – and 41% use of its $585,000 surplus, which contributes another 11% of total operating revenue.

West Cape May raised its local purpose tax 4.4% in 2023 on a general fund budget of $3.8 million. The town also maintains a water/sewer utility budgeted at $1.6 million.

West Cape May obtains policing through an agreement with Cape May and is a water customer of the city, as well. Debt service at $556,000 runs at 14% of general fund revenues, which puts the town at the median level for the county’s island communities. West Cape May used a low 37% of its surplus to balance the budget.

Overall, the eleven island communities have total general fund expenses of $321 million, with combined tax levy revenues of $200 million. They started the year with a combined $69 million in surplus balances and used just under 50%, on average, to balance their budgets.

Mainland Towns

The five mainland towns consist of the four townships and Woodbine. These towns are home to two-thirds of the county’s permanent population, according to the 2020 census. They provide services based on tax revenue from approximately 17% of the county’s valuation total.

This is the second year in which Upper Township led all county municipalities in the percentage increase in its local purpose tax rate.

Budgets are tight and the room for error, given fewer alternative sources of revenue, is smaller.

Only two of the five municipalities make use of self-financing utilities. The combined general fund budgets and utility budgets of the five towns for 2023 is $89.4 million, the largest portion of that total being $83 million in combined general fund expense for which the towns charge a combined total of $47 million in tax levy.

Upper Township leads the 16 towns with its 11.1% local purpose tax rate increase. A large and critical source of funds for the township is the energy tax receipts that the state rebrands as state aid, but this is largely a static number, so annually rising expenses turn into a burden the tax levy must cover.

The state aid still allows the township to have the lowest level of percentage reliance on tax dollars to fund its budget; roughly 33% or one-third of the budget is dependent on taxes.

This is the second year in which Upper Township led all county municipalities in the percentage increase in its local purpose tax rate.

Dennis Township’s local purpose tax for 2023 went up by 5.2%, moving from $0.230 to $0.242 per $100 of assessed value. The $5.9 million general fund budget calls for a tax levy of $2.2 million, uses $750,000 of a total $2 million surplus, and benefits from energy tax receipts of $1.7 million under the heading of state aid.

Debt service is $1.16 million or almost 20% of total revenue. The township does not make use of self-financing utilities. The cap bank balance is small – at $150,000 – meaning it provides little cushion if the township ever had to exceed its taxation cap in order to fund a future budget.

Woodbine is the third of the three county municipalities that saw no local purpose tax rate increase. The borough makes use of utilities for water/sewer and for its airport budget.

The borough’s general fund budget is $3.5 million, with another $1.1 million in the budgets of its two utilities. The borough has a $1.2 million surplus balance of which it used $559,000 in the 2023 budget. For 2023, Woodbine’s tax rate – at $0.233 – is the lowest among mainland municipalities.

This was a challenging year for Middle Township. A budgeting error in 2022 forced an emergency appropriation that the township cleared before the close of that budget year. Clearing that appropriation may have cost the township resources that could have bolstered its surplus balance.

The 2023 budget calls for a 9.2% increase in the local purpose tax rate, raising the rate almost 5 cents. Confronted by hikes in health care and pension costs, the township also had a $900,000 hole in its budget caused by the expiration of federal relief dollars, which it had budgeted as revenue for the previous two years. The combination of tax levy and surplus used represent over 70% of total expected revenue.

Despite the 9.2% increase in the tax rate, the township still used 96% of its surplus balance as anticipated revenue in the budget. It was also not able to add to its anemic cap bank balance of $114,000. There is not much room for error in the task of having sufficient funds unexpended this year to replenish the surplus, which currently stands after the budget adoption at $66,000. Middle has a sewer utility budgeted at $5.5 million for 2023.

Lower Township has a $33.3 million budget for 2023 with no utilities. Its budget imposes a 3.68% increase in the local purpose tax rate, with a total levy expected at $23.1 million or 69% of the budget from tax dollars.

The township uses 52% of its healthy $8.4 million surplus as revenue in the 2023 budget. With the surplus amount used, the budget is 85% supported by the combination of the levy and the surplus, leaving only 15% to other sources of revenue.

The five mainland towns started the year with a combined $17 million in total surplus, with almost half of that being the $8.4 million balance in Lower Township. On average, they use a higher percentage of their surplus dollars as revenue in the annual budget than do the island communities.

Contact the author, Vince Conti, at vconti@cmcherald.com.